Income Tax Planning

Strategies to help lower your lifetime tax bill.

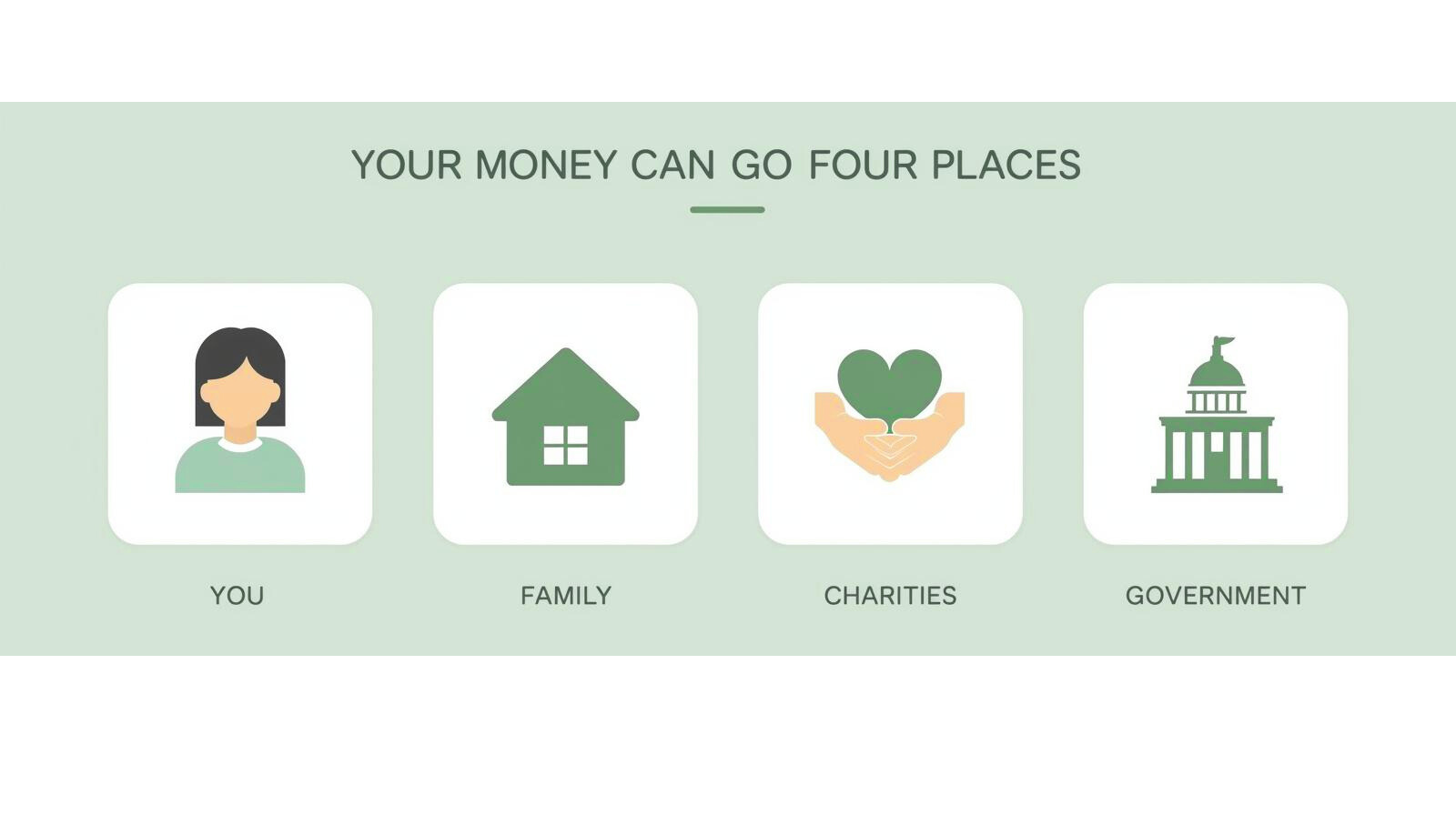

Your money can ultimately go to four places: you, your family, charities, or the government. Thoughtful income tax planning helps you decide ahead of time where you want it to go and then build a plan around that choice.

From there, we review your tax returns and investment accounts to uncover opportunities such as tax‑efficient investing, smart asset location, tax‑loss and capital gain harvesting, and Roth conversions. We also plan around Social Security, Medicare, IRMAA, NIIT, and the widow’s penalty so you can reduce surprises and keep more of what you’ve worked for.

Tax Planning

We help lower taxes over your lifetime with smart investing, tax‑efficient withdrawals, and proactive planning for surprises like IRMAA, NIIT, and the widow’s penalty, using AI‑powered analysis to uncover opportunities you might otherwise miss.

-

Common tax mistakes in retirement include ignoring RMDs, taking money from the wrong accounts first, forgetting that Social Security and investment income can be taxable, and not adjusting withholding or estimated payments. We regularly review these pressure points with clients so they can avoid surprise tax bills, penalties, or missed opportunities to smooth taxes over their lifetime.

-

You generally pay less tax in retirement by planning ahead: using a mix of account types (pre‑tax, Roth, and taxable), coordinating the order of withdrawals, and being thoughtful about Roth conversions before required minimum distributions (RMDs) start. We help Women in STEM and Retirees design “tax‑smart retirement income” strategies so more of what you saved stays working for you instead of going to unnecessary taxes year after year.

-

There is no special “retirement tax bracket,” you pay federal and state income tax based on the same IRS tax brackets as everyone else; the difference is how your retirement income is taxed (Social Security, pensions, IRAs, Roth, brokerage, etc.). In our planning work, we estimate your future retirement income, map it onto current tax brackets, and test different strategies so you can see how choices like Roth conversions, withdrawal order, or part‑time work may affect your taxes over time.

-

Your filing status affects your tax brackets, standard deduction, and eligibility for credits. Head of household status is available if you are unmarried and support a dependent. Married couples can often save by filing jointly, but sometimes separate returns make sense. Review your living situation and dependents to select the best status for your situation.

-

You may qualify for credits like the American Opportunity Credit or Lifetime Learning Credit, which can reduce your tax bill for tuition and related expenses. Student loan interest is also deductible up to a certain limit. Save receipts and Form 1098-T from your school to claim these benefits.

-

All income, including from side gigs or online sales, must be reported—even if you do not receive a 1099 form. Keep detailed records of your earnings and related expenses. You may need to pay self-employment tax and make estimated tax payments throughout the year.

-

Long-term capital gains (assets held over a year) are taxed at lower rates than short-term gains. Use tax-loss harvesting to offset gains with losses, and consider holding investments longer for better rates. Plan sales strategically, especially near year-end.

-

If you are age 73 or older, you must take RMDs from traditional IRAs and most employer retirement plans. These withdrawals are taxed as ordinary income, and failing to take them can result in steep penalties. Plan your withdrawals to manage your tax bracket and consider charitable qualified distributions.

-

Watch for errors like missing or incorrect Social Security numbers, math mistakes, and forgetting to sign your return. Double-check bank details for direct deposit and ensure all forms are included. Filing electronically can help catch many common errors.

-

Maximize contributions to retirement accounts, HSAs, and FSAs. Consider charitable donations, bunching deductions, and tax-efficient investment strategies. Review your portfolio for opportunities to defer income or accelerate deductions, and consult a Certified Financial Planner (CFP) or tax professional for advanced planning.

-

Equity compensation can be a powerful wealth builder, but the tax rules are confusing. I help you map out vesting schedules, expiration dates, and tax treatment so you know what you own and what each choice means. Together we can create a plan for when to exercise, sell, or hold, how to diversify concentrated positions, and how to line up your decisions with both your cash flow needs and your long term goals.

-

Tax smart withdrawals can help your money last longer by keeping more dollars working for you instead of going straight to taxes. Depending on your situation, that might mean drawing from taxable accounts first, blending different accounts, or using strategic Roth conversions before required minimum distributions begin. Together we design a coordinated plan so you are not pulling from “wherever feels easiest,” but from the places that support your long term goals.

-

High earners often have more control over when and how they recognize income than they realize. We look at retirement plans, equity compensation, charitable giving, and account types to find ways to shift income, use deductions, and build tax flexibility. Over time, a series of thoughtful decisions can reduce the lifetime tax drag on your wealth.