Retirement Income Planning

Watch this video showing how our planning tools turn your questions into clear, visual answers. 👈

"What happens if I retire at 62 instead of 65?" 💼 "Can I afford to help my kids and travel?" ✈️

We don't guess, we model it. 📊

Designing Your Ideal Retirement, One Smart Decision at a Time

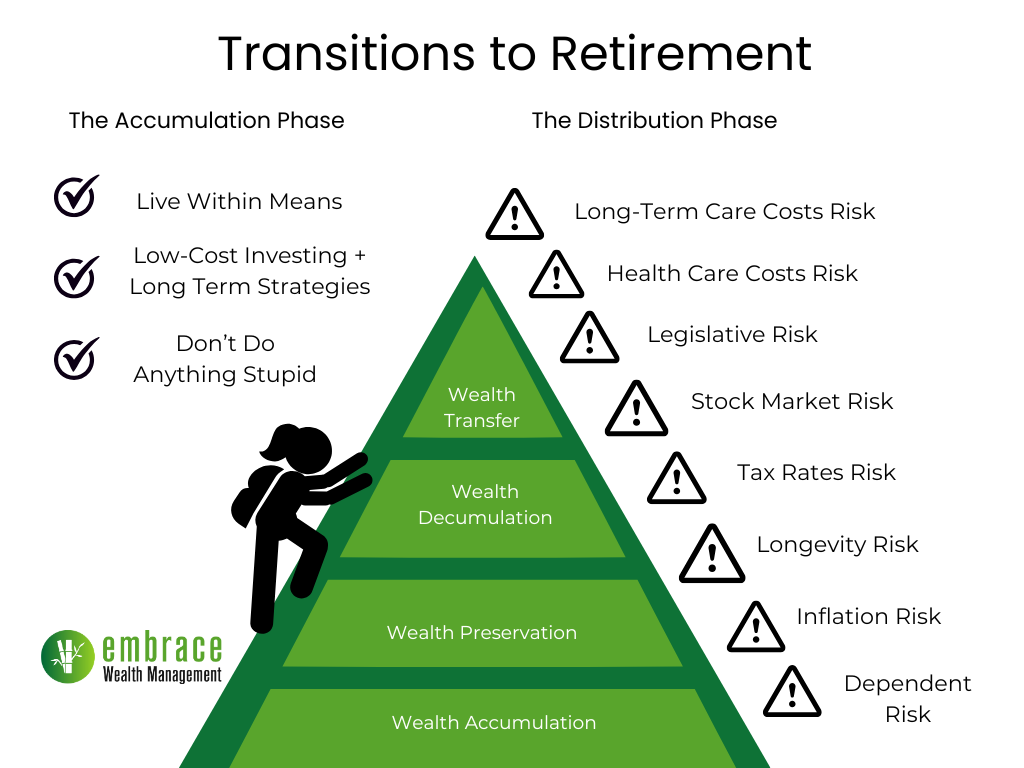

We help you align your investments, retirement income, taxes, estate planning, and insurance. So every financial decision supports confident, independent living and a secure legacy for the people and causes that matter most.

Planning Your Ideal Life 💸

What do you dream of doing in retirement? We’ll help you build a spending plan that supports travel, hobbies, new adventures, and time with the people you love.

Making Your Money Last 💰

We’ll look for ways to maximize your retirement income, Social Security strategies, investment planning, and smart use of tax‑advantaged accounts so your savings can go further.

Healthcare in Retirement 💊

We’ll walk through Medicare options, supplemental coverage, and proactive steps to manage healthcare costs, so you feel more prepared for the future.

Building Your Legacy 🏡

Estate planning matters. We’ll coordinate with your attorney to help you create or update documents, name beneficiaries, protect what you’ve built, and support the causes and people you care about.

Staying Active and Engaged 🎉

Retirement is a time to flourish. We’ll talk about staying healthy, connected with loved ones, and involved in community or volunteer activities, so your plan supports a full, meaningful life.

-

Yes, You can roll over your 401(k) to a traditional IRA without any taxes or penalties, as long as you follow the IRS rules. The easiest and most common way is a direct rollover, where your retirement funds move straight from your 401(k) to your IRA. This way, you never touch the money yourself, so there aren’t any tax consequences or early withdrawal penalties.

If you decide on an indirect rollover, the check comes to you, but your employer withholds 20% for taxes. You’ll need to deposit the whole amount (not just what you received) into your IRA within 60 days to avoid taxes and the 10% penalty if you’re under 59½. Missing the deadline can trigger taxes and penalties, so direct rollovers are usually safest and simplest.

-

Women tend to live longer than men, which means your retirement savings may need to stretch further. Start by reviewing your spending needs and creating a realistic budget that includes healthcare, housing, and leisure. Consider working with a financial planner to develop a sustainable withdrawal strategy, such as the 4% rule or a dynamic withdrawal method. Factor in inflation, unexpected expenses, and possible long-term care needs. Revisit your plan annually and adjust as your circumstances or market conditions change.

-

Delaying Social Security benefits until age 70 can significantly increase your monthly payments, but the right claiming age depends on your health, income needs, and marital status. Understand how your past earnings, spousal benefits, and survivor benefits impact your payout. If you have a STEM career with higher late-career earnings, this can boost your benefit calculation. Be mindful of how part-time work or other income sources may affect your taxes and Social Security income. Consulting with a retirement specialist can help you optimize your claiming strategy.

-

Healthcare is often one of the largest expenses in retirement, so factor in premiums, out-of-pocket costs, and potential long-term care. Consider supplemental insurance (like Medigap or Medicare Advantage) and review your coverage annually. Health Savings Accounts (HSAs) can be a tax-efficient way to save for medical expenses if you are not yet on Medicare. Explore long-term care insurance options early, as costs rise with age and health changes. Building a dedicated healthcare fund can provide peace of mind.

-

Diversify your income sources—combine Social Security, retirement accounts, pensions, and possibly annuities. Consider part-time work, consulting, or monetizing hobbies for additional income if desired. Review your investment allocation to balance growth and safety, shifting to more conservative investments as needed. Maintain an emergency fund for unexpected expenses. Regular check-ins with a financial planner to help ensure your plan remains on track as you age.

-

Understand how withdrawals from different accounts (401(k), IRA, Roth, brokerage) are taxed, and plan your distributions to minimize your tax burden. Consider strategies like Roth conversions or drawing from taxable accounts first. Be aware that Social Security benefits may be taxable depending on your total income. Take advantage of tax credits and deductions available to retirees. Work with a tax professional to optimize your strategy and avoid surprises.

-

Ensure your will, power of attorney, and healthcare directives are up to date. Consider setting up trusts if you have complex family needs or wish to control how assets are distributed. Review beneficiary designations on retirement accounts and insurance policies regularly. Charitable giving, whether through direct gifts or donor-advised funds, can be part of your legacy plan. Consulting with an estate attorney ensures your wishes are clearly documented and legally sound.

-

Organize all financial accounts, passwords, and important documents in a secure, accessible place. Understand your rights to survivor benefits, pensions, and Social Security. Seek professional advice before making major financial decisions during periods of grief. Build a support network of trusted friends, family, or advisors. Financial empowerment and awareness are key to maintaining independence and security.

-

Stay invested, but adjust your risk tolerance to reflect your age and needs. Focus on income-generating investments such as dividend stocks, bonds, or annuities. Consider real estate or other passive income streams if appropriate. Join investment communities or educational groups tailored for women to keep learning and stay engaged. Periodically rebalance your portfolio to maintain your desired asset mix.

-

Many retired women find fulfillment in giving back, whether through volunteering, charitable donations, or supporting family members. You might consider setting up a donor-advised fund, making regular charitable contributions, or volunteering your time and expertise to local organizations. If helping family is a priority, be clear about your own financial boundaries to avoid jeopardizing your long-term security. Estate planning tools, such as gifting strategies or trusts, can help you manage how and when you provide support. Giving back can offer a sense of purpose and connection, but always ensure your generosity aligns with your financial plan and retirement goals.

-

It is wise to seek guidance from Certified Financial Planners (CFP), retirement specialists, or reputable financial institutions that understand the unique needs of women in retirement. Many banks, investment firms, and nonprofit organizations offer educational workshops, online resources, and one-on-one consultations. Community centers, local senior groups, and online forums can provide both practical advice and social connection. Staying informed through reliable sources and building a network of supportive peers can help you navigate financial decisions and enjoy a more secure, fulfilling retirement.

-

Many women quietly worry about outliving their money. We build a retirement income plan that includes Social Security, pensions or annuities if available, and withdrawals from savings in a tax aware way. Then we stress test that plan for long life, market swings, and health care costs so you can see how your retirement paycheck holds up and make informed choices about spending, work, and timing.

-

There is no single number that works for everyone. The amount you need depends on your lifestyle, location, health, and how much you want to spend on travel, family, and hobbies. I help you translate those pieces into an annual spending target, then into a savings and investment plan, so you can see whether you are on track and what adjustments might help.

-

The right claiming age depends on your health, work plans, marital history, and other income sources. For many women, especially those who may live longer, waiting can provide higher lifetime benefits, but it is not always the best choice. We run side by side scenarios so you can compare different claiming ages and coordinate your decision with your broader retirement income plan.

-

A retirement paycheck usually comes from several sources working together. We look at guaranteed income, like Social Security and pensions, plus withdrawals from savings and investments, and we plan the order and timing in a tax smart way. The aim is a stable, sustainable flow of income that supports your lifestyle today while staying mindful of the future.

-

The best order depends on your tax bracket now, your expected future brackets, and your goals for leaving money to others. Many plans use a blend, drawing from taxable accounts first in some years, traditional accounts in others, and saving Roth assets for later or for heirs. We review your full picture and build a withdrawal roadmap so each year feels intentional, not random.